Financial update of september

UPDATE DI SETTEMBRE

In recent weeks, we have witnessed interesting developments in the financials debt market.

Overall, the quarterly results season confirmed the health of the European banking system, in terms of profitability and fundamentals (both in terms of asset quality and regulatory capital). Net interest income on average grew by around 30% year-on-year, the cost of credit remained anchored at the levels of recent quarters, and capital continued to benefit from the organic ability to generate profits, while offering attractive returns to shareholders (RoE averaged 12% in the quarter, with peaks of 14.7% in Italy and 13% in Spain).

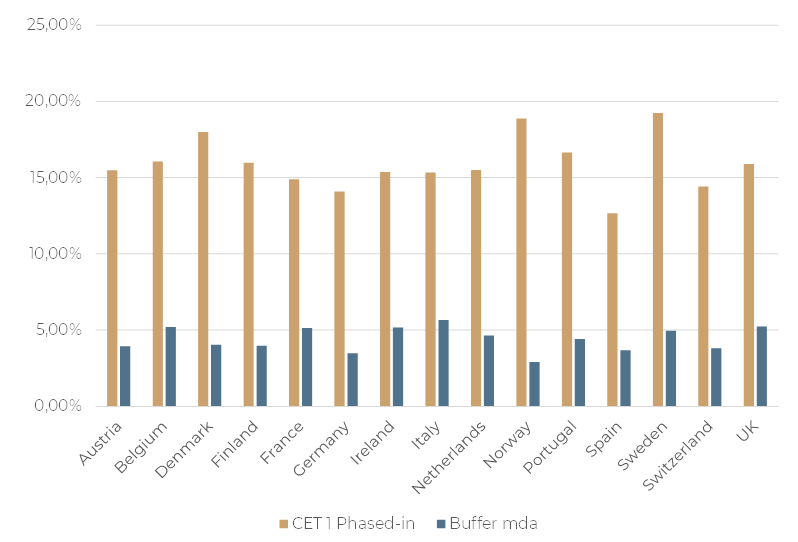

On capital side, according to our calculations, the average CET1 is above 15% with a capital cushion against regulatory requirements (MDA buffer) of 470 bps.

AVERAGE LEVEL OF CAPITAL PER COUNTRY AND BUFFER VS MDA REQUIREMENT

Source: Valori AM on corporate data as of 31/08/2023.

On the regulatory front, some European countries have announced new taxes on bank profits, in an attempt to transfer part of the benefit of rising rates from the banks to the community, as the return on deposits remains very low. Italy was the latest country to join the group of governments that are imposing taxes on banks in various ways (UK, Spain, Netherlands), with a 40% tax on annual growth in net interest income exceeding the 8% threshold: a measure still under discussion and which initially weakened market confidence on the equity market, but without any significant impact on the fixed income market.

Activity on the primary market, after the usual summer break, confirmed investors’ interest in the Additional Tier 1 asset class, with around $5.2bn of new issues from systemic issuers such as BBVA, ERSTE, INTESA, KBC, BNP and particularly attractive coupons (average above 8%).

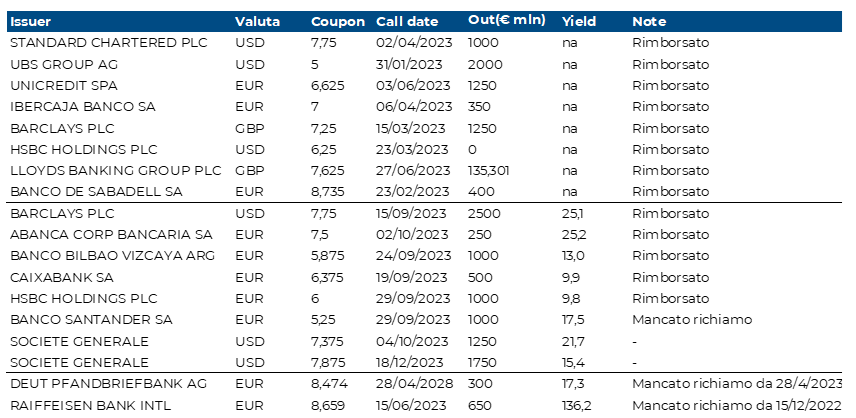

The AT1 market also saw several issuers proceed with the redemption of AT1s on the first call date in recent months (Barclays, Abanca, BBVA, Caixa, HSBC), with the exception of Santander and Zürcher Kantonalbank.

AT1: NEXT CALLS

Source: Valori AM on Bloomberg data as of 12/09/2023.

On Santander, we point out that this is certainly nothing new, as it had already happened in March 2019 when the issuer opted not to call an AT1 bond (coupon 6.25%), surprising the market with this decision (given that the bank had apparently financed the redemption by issuing a new $1.2bn AT1 the previous month). The coupon was resetted to 5.481% and the bond, with a call exercisable quarterly, was called in March 2020.

This time, unlike in the past, the market did not react negatively to the news: the bond’s coupon will rise from 5.25% to 8.20% (at current market conditions) and the quarterly call leaves the issuer with the option of a possible recall in the coming months.

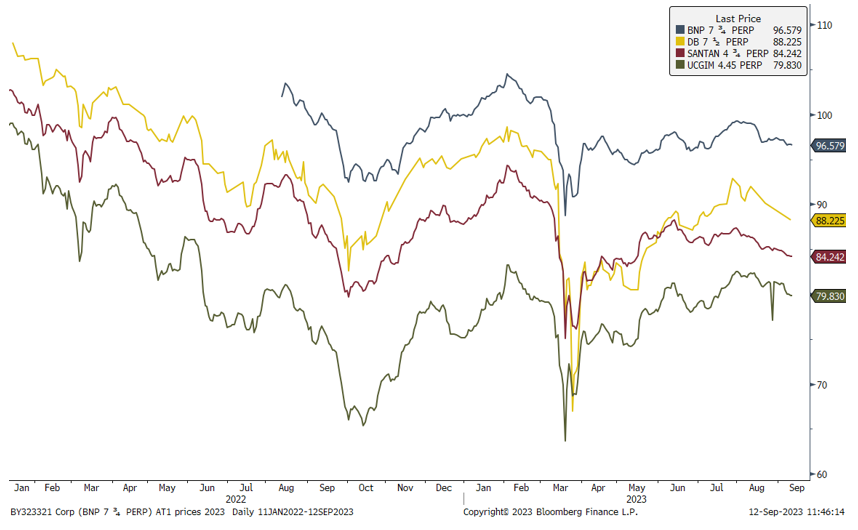

PERFORMANCE BOND AT1

Source: Bloomberg, data as of 12/09/2023.

We therefore do not see any long-term effects on the price levels of Santander’s other AT1s or more generally on the AT1 market arising from this news.

On the contrary, the flow on the primary deals , the good series of recalls on the AT1 market or the buy-back offers launched in conjunction with new issues (as in the case of Intesa) have improved market sentiment. In terms of valuation, AT1s trade at a discount to the corporate high-yield market, and as the chart below shows, many instruments have not yet fully recovered from last March’s drawdown.